How AI-Driven Document Understanding Transforms Mortgage Processing

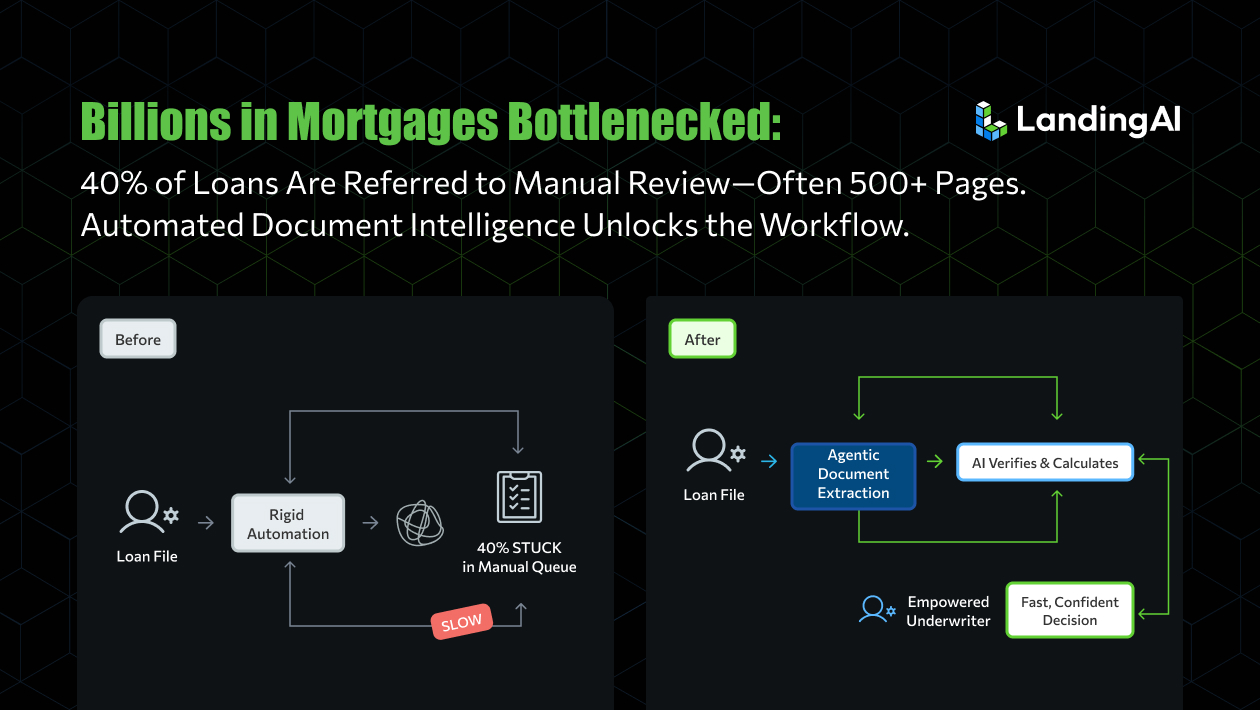

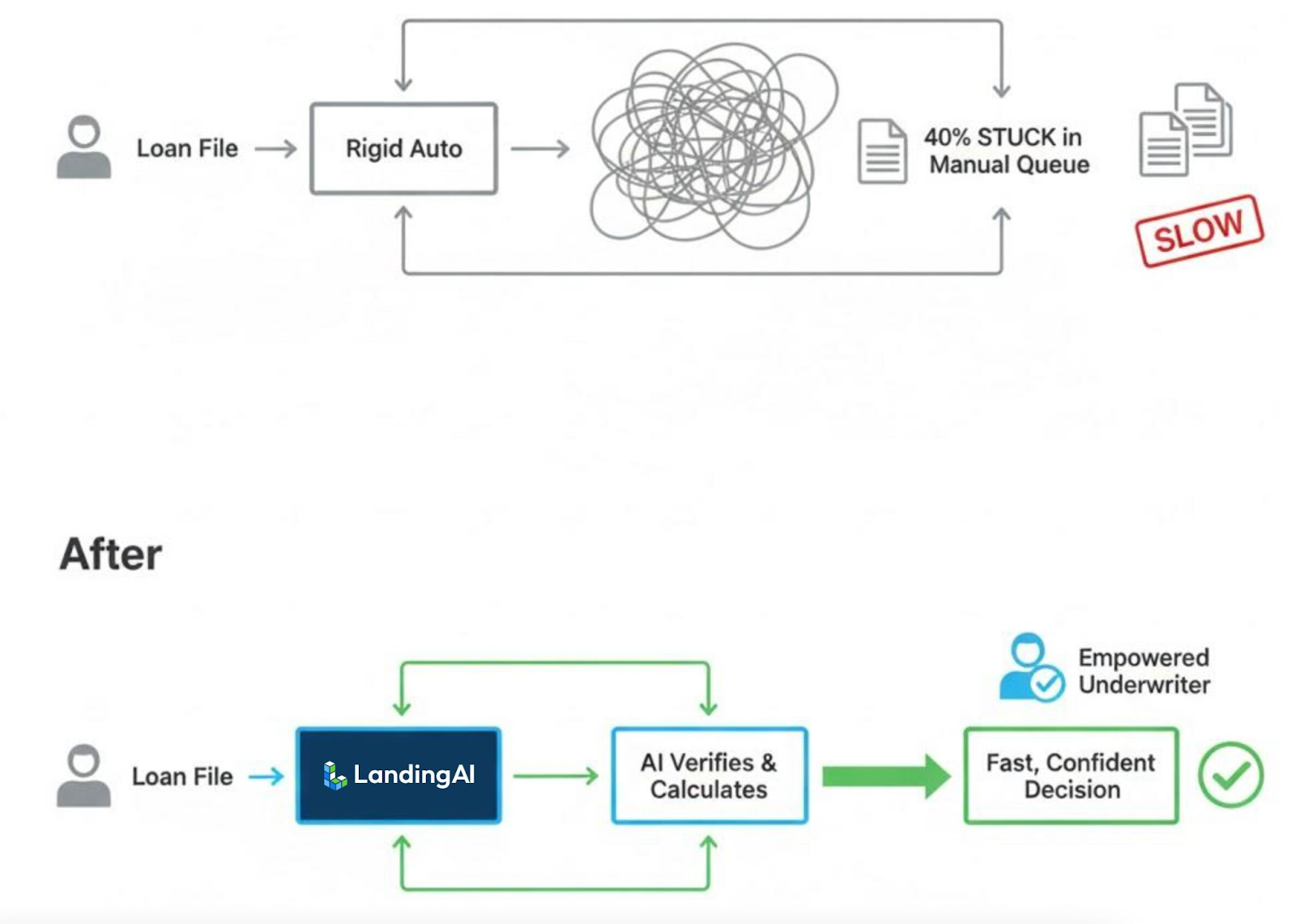

40% of Loans Are Referred to Manual Review—Often 500+ Pages. Automated Document Intelligence Unlocks the Workflow.

In this blog, we’re exposing the multi-billion-dollar bottleneck in the mortgage industry. It’s not about interest rates; it’s about the massive, hidden pile of “complex” loans that your automation can’t handle.

These are the loans that get kicked out of the fast lane and dumped into a manual queue, leaving your most valuable customers to wait… and wait… and wait.

But first, let’s see what concerns every lender:

Only 60% of loans are “simple” enough for a clean automated approval from Fannie Mae’s or Freddie Mac’s systems.

The other 40% (self-employed, jumbo loans, rental properties) are “Referred” to a manual underwriter, immediately adding days or weeks to the process.

A single complex loan file can be 100-500+ pages of tax returns, bank statements, W-2s, and title reports.

Guidelines are fragmented across Fannie Mae, Freddie Mac, and each lender’s own “stricter” overlays, which change annually.

Up to 50% of detected fraud involves fabricated documents—like Photoshopped bank statements—that look real to a basic scanner but break on simple math.

The Customers Who Never Were

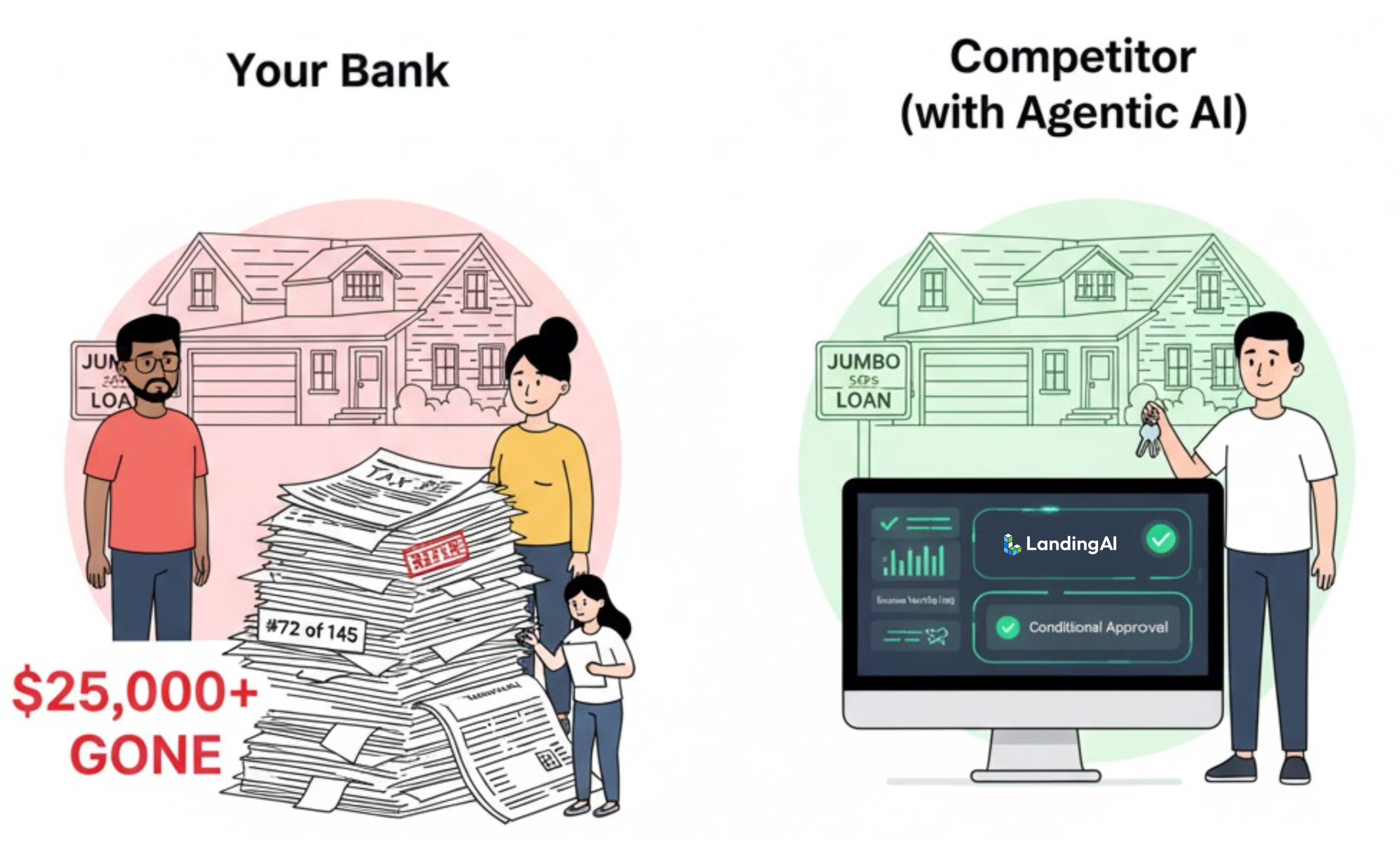

Mark and Julia found their dream home on Saturday. They’re your perfect high-value clients: Mark is a self-employed consultant, Julia is a W-2 doctor, and they need a “Jumbo Loan” for their Bay Area home.

Your loan officer spent $450 to acquire them. They uploaded their life’s history on Monday morning.

Your automated system (DU/LPA) took one look at Mark’s 100-page tax return and Julia’s RSU income and immediately punted.

Result: “Refer.”

Their file lands in your senior underwriter’s queue. They are #72 of 145.

Your competitor, using an agentic AI, verified Mark’s complex Schedule C income and Julia’s RSUs in under an hour. They got conditional approval by Tuesday.

Mark and Julia’s $1.1M loan? Gone.

Their lifetime value? $25,000+. Gone.

When “Automated Underwriting” Isn’t Automated

Your system didn’t fail. It did exactly what it was designed to do: identify a loan it can’t handle.

Now, your $150k/year senior underwriter, Anna, opens the file. She is now the most expensive data-entry clerk at your company.

Her next four hours look like this:

Open Mark’s tax return (PDF).

Open her personal Excel sheet (the one she built herself because your system can’t do this) to manually calculate his 2-year average Schedule C income.

Open Julia’s paystub (PDF), W-2 (PDF), and tax return (PDF).

She manually compares all three, highlighting a 10% discrepancy that will require a “letter of explanation.”

Open their bank statements (PDF). She’s not just checking the balance; she’s manually checking the math on the deposits vs. the income she just calculated.

She isn’t making a high-level risk decision. She’s drowning in repetitive, “very time-consuming” verification.

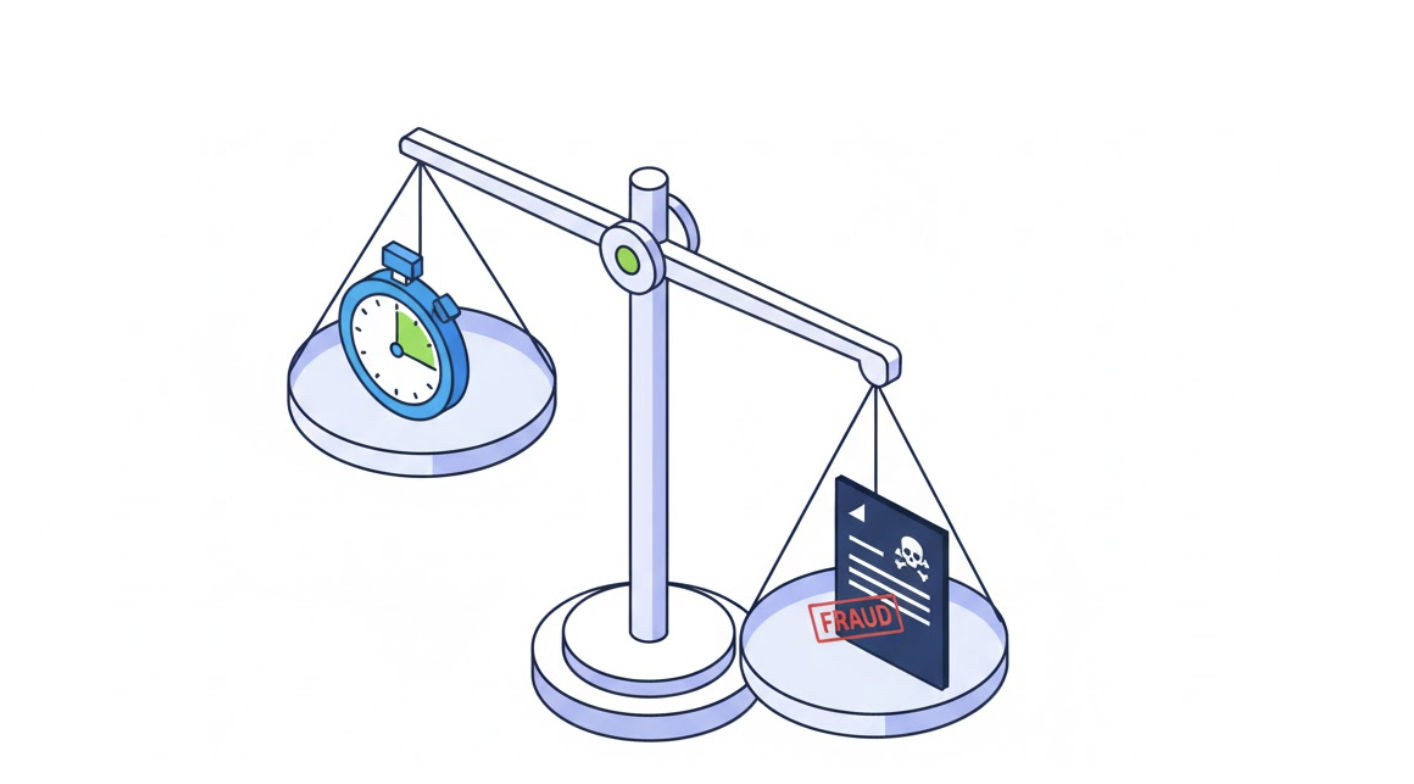

The Underwriting Catch-22

You can’t go faster; the risk is brutal.

In 2023, fraudulent loan applications cost the industry billions.

“Move too fast, you buy a fraudulent loan. Move too slow, you lose the customer.”

Rigid automation creates this false choice: speed or accuracy.

Neither side wins.

When Six Documents Become Too Many

What did Mark and Julia actually upload?

Paystubs (30 days, multiple formats)

W-2s (2 years)

1040 Tax Returns (2 years, all schedules)

Bank Statements (2 months)

Preliminary Title Report (from a 3rd party)

Appraisal Report (another 3rd party PDF)

Every single document must be manually cross-referenced. A simple OCR can rip text off a page, but it can’t understand it.

It can’t compare the paystub to the W-2.

It can’t calculate the qualifying income from a Schedule C.

It can’t validate that the bank statement’s transactions actually add up.

When “Refer” Means “Risk”

Ironically, that manual queue isn’t just slow; it’s your biggest compliance vulnerability.

Fraudsters know your automated systems are rigid. They create fabricated paystubs or Photoshopped bank statements that look perfect. They know your senior underwriter is on her 200th PDF of the day and might miss the fact that the numbers just… don’t… add… up.

A single missed fraud? A $500,000+ loan you have to discharge. A costly buy-back from an investor.

How Agentic AI Changes Everything

The smartest lenders aren’t just digitizing old steps; they’re automating the thinking.

AI-powered document intelligence can:

Verify income across paystubs, W-2s, and 1040s instantly.

Calculate complex income (self-employed, RSU, bonus) using the correct GSE formulas.

Detect fraud, like a bank statement where the math is wrong.

Check the appraisal comps to see if they’re really within 1-2 miles.

Read the title report and flag a new judgment lien.

This isn’t just text extraction. It’s an AI that acts like a junior underwriter, prepping the entire file for a final human decision.

Building a Better Underwriting Flow

Manual “Refer” queues are creating three massive problems:

You’re losing your best customers (the complex, high-value ones) to faster competitors.

You’re paying six-figure salaries for experts to do repetitive data verification.

Your manual process is a gateway for fraud that preys on human fatigue.

Winning teams are re-engineering their workflow. They do this:

Automate Verification, Not Just Extraction: Build logic that cross-checks documents and flags inconsistencies.

Handle the 40%: Implement systems that “understand” and can calculate Schedule C and RSU income.

Empower the Human: Create clear workflows that send the AI’s analysis (not just the raw data) to the senior underwriter for a final, fast decision.

Your Next Move – Turning the Bottleneck into Opportunity

The “Refer” pile of complex loans shouldn’t be seen as a burden – it should be seen as a goldmine of opportunity. These 40% of loans are often the biggest loans, made to the most financially active customers (self-employed professionals, real estate investors, affluent buyers in pricey markets). In other words, exactly the customers you want. If you’re losing them due to slow manual processes, it’s time to act.

Agentic AI solutions like LandingAI’s Agentic Document Extraction (ADE) are game-changers in this space. They combine computer vision, natural language understanding, and contextual reasoning to read and interpret complex mortgage documents with human-like comprehension. For example, ADE doesn’t just OCR a tax form – it knows it’s a Schedule C with specific meaning, and it can apply the correct income calculations automatically. It “understands” what the document means, not just what it says.

In the end, speed and quality in mortgage underwriting are no longer at odds. The fastest experience can also be the most reliable when it’s powered by intelligent automation. Lenders who embrace these tools are already winning market share from those who don’t. They’re turning the old bottleneck into a competitive advantage – marketing their faster approvals and snagging those valuable “Mark and Julia” customers of the world.

Ask yourself: How long is your “Refer” queue right now? And what is it costing you – in customer goodwill, in lost loans, in elevated fraud risk? If the answer is uncomfortable, it’s time to explore solutions like LandingAI’s ADE to transform your underwriting operations.